(Bloomberg) — Cracks are finally appearing in the euro zone’s labor market after years of unexpected resilience — spurring the European Central Bank to lower interest rates more speedily.

Most Read from Bloomberg

Despite still record-low joblessness following the inflation shock and a struggling economy, policymakers see signs of a shift that’s helped persuade them to back another reduction in borrowing costs this week.

While lacking the dual mandate through which the Federal Reserve targets both price stability and full employment, a jolt to Europe’s jobs market can nevertheless have a significant impact on the ECB’s inflation outlook.

With major companies like BASF SE and Thyssenkrupp AG already offloading staff, some officials fear a sudden deterioration that could further rattle a region teetering on the brink of a recession.

“I think they’re going to cut in October and will continue cutting — even though some of the hawks say there’s no automaticity in the easing cycle,” said Soeren Radde, an economist at Point72. “They’re on that track and they need to be. The key concern is really the labor market.”

It was only July when President Christine Lagarde touted the strength of Europe’s jobs market as a reason that the ECB could “take time to gather new information” when setting monetary policy. That time now appears to have run out.

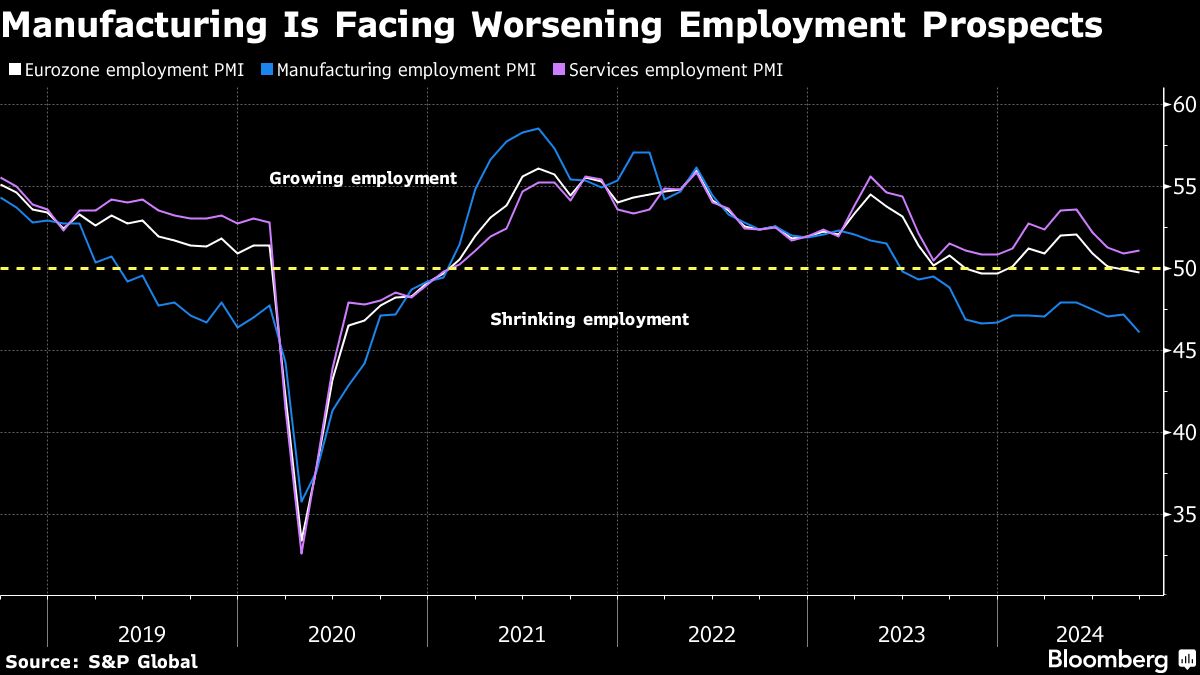

For now, data only point to a gentle cooling rather than a rapid downturn. But employment growth slowed to just 0.2% in the second quarter and the share of vacant jobs dropped to 2.6% in the same period from a peak that topped 3%. Surveys like the monthly polls of purchasing managers by S&P Global also paint a worsening picture.

“The slowdown in vacancies and pace of hiring are signals that should be paid attention to — this was clearly an important motivation for the Fed in opting for 50 basis points,” said Michala Marcussen, group chief economist at Societe Generale, referring to the US rate cut in September.

Portuguese central-bank chief Mario Centeno, a labor economist by training, sees early indications of a softening in the euro area, with “some flashing more urgent warning signs than others, but all pointing toward a potential reversal in the labor market.”

Even hawkish officials acknowledge the issue. Executive Board member Isabel Schnabel thinks less appetite for personnel makes a sustainable fall of inflation to the 2% target more likely. Latvia’s Martins Kazaks has flagged the risk of a tipping point, when some firms may start to undo earlier hoarding of staff as the economy disappoints.

“Then there could be some kind of a snowball effect,” he warned.

Manufacturing is a key problem — squeezed by weak Chinese demand and competitive disadvantages at home. While that’s been the case for a while, a popular theory was that firms retained staff regardless in case rehiring them if needed later was hard.

Some firms appear to be losing confidence in an economic rebound. A case in point is Volkswagen AG, which is considering closing plants in Germany for the first time. Plans for cutbacks in the sector — including at Continental AG — have continuously trickled in. Hesitant consumers, meanwhile, mean services haven’t picked up the slack.

As a result, economists at Goldman Sachs predict that the euro-area unemployment rate will rise to 6.7% over the next several quarters. They say a worse outcome is possible if the economy underperforms — supporting their case for rate cuts at every meeting starting this week and until the deposit rate reaches 2%, from 3.5% now.

Bolstering arguments for faster easing is the fact that a softer jobs market typically also translates into more meager pay rises and thereby less inflation.

“If labor markets continue to cool, workers could accept more modest wage increases in upcoming wage renegotiations in exchange for job security,” economists at Barclays wrote recently.

The ECB’s assumption that it will sustainably reach its 2% inflation target in the second half of 2025 is based on a slowdown in wage gains. But it also doesn’t want the labor market and advances in pay to moderate too much.

Chief Economist Philip Lane said last week that a stronger jobs market “increases the likelihood of hitting the inflation target rather than being chronically below,” and that “wage increases would be more target-consistent in the coming years” than pre-Covid.

“The labor markets in the euro area still look quite resilient, but there are clear signs of a softening,” said Karsten Junius, an economist at Bank J. Safra Sarasin. “The ECB should also react to that and make sure that there’s no real slump with significantly rising unemployment. This also suggests front-loading of interest-rate cuts.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Read the full article here