US Dollar (DXY) Analysis

- Rising price pressures and employment costs elevate USD and yields ahead of FOMC

- US dollar index tests key upside level but markets may be in for disappointment

- Major risk events ahead: FOMC, ISM PMI, ADP and JOLTs data, NFP on Friday

- Get your hands on the U.S. dollar Q2 outlook today for exclusive insights into key market catalysts that should be on every trader’s radar:

Recommended by Richard Snow

Get Your Free USD Forecast

Rising Prices and Employee Costs Demand the Fed’s Attention

The three-month percent rise in civilian worker’s total compensation rose above the maximum estimate from economists/analysts. The data for the three-month period ending in March rose 1.2% after rising 0.9% in the three months before that, beating estimates of 1%.

The number is of less significance than the surprise element itself and when you tally this up alongside accelerating month-on-month core inflation, questions start to be raised around just how restrictive the current policy stance really is.

Source: Bureau of Labor Statistics

Considering the Fed can still point to signs of continued disinflation, despite recent challenges, suggests the committee may repeat that more work needs to be done and that policy setters will look to in coming data.

The summary of economic projections are not due until June meaning the Fed is more likely to bide its time until then, avoiding the risk of jumping to conclusions. Jerome Powell may simply repeat what he said on the 17th of April concerning recent price pressures, “the recent data have clearly not given us greater confidence and instead indicate that is likely to take longer than expected to achieve that confidence”.

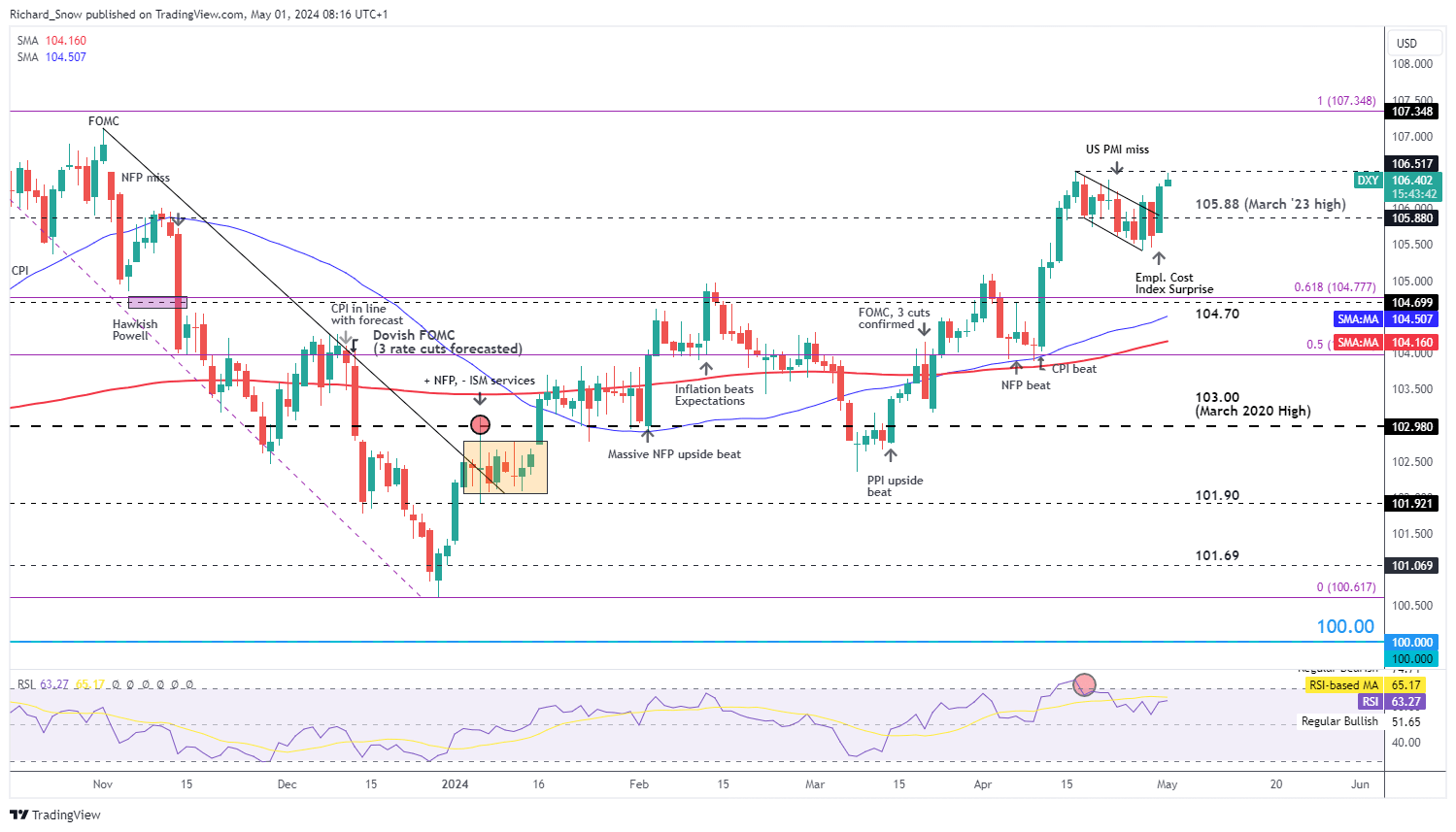

USD Tests Key Resistance Level but Markets May be in for Disappointment

The US dollar trades higher in the lead up to the FOMC meeting after the boost in employment costs yesterday. However, it is worth noting that each of the three previous Fed meetings ended with a lower dollar, so dollar bulls ought to keep that in mind.

DXY tests the yearly high of 106.51, revealing a slight intra-day aversion for the level in the early London session as traders jockey for positioning. The dollar appears to be making an attempt to breakout from the descending channel which emerged after the Israel-Iran de-escalation. In the absence of a change in the wording in the statement to reflect the possibility of a rate hike, I believe the bar to upside momentum remains rather high for now. That being said, a hawkish tone from the Fed may be enough to see marginal gains for bulls after the announcement. A level of interest to the downside emerges at the March 2023 high of 105.88.

Stay attentive to data ahead of the meeting, for example, the ADP and JOLTs data as they inform the market’s perceptions of the labour market ahead of NFP on Friday.

US Dollar Basket (DXY) Daily Chart

Source: TradingView, prepared by Richard Snow

Looking for actionable trading ideas? Download our top trading opportunities guide packed with insightful tips for the second quarter!

Recommended by Richard Snow

Get Your Free Top Trading Opportunities Forecast

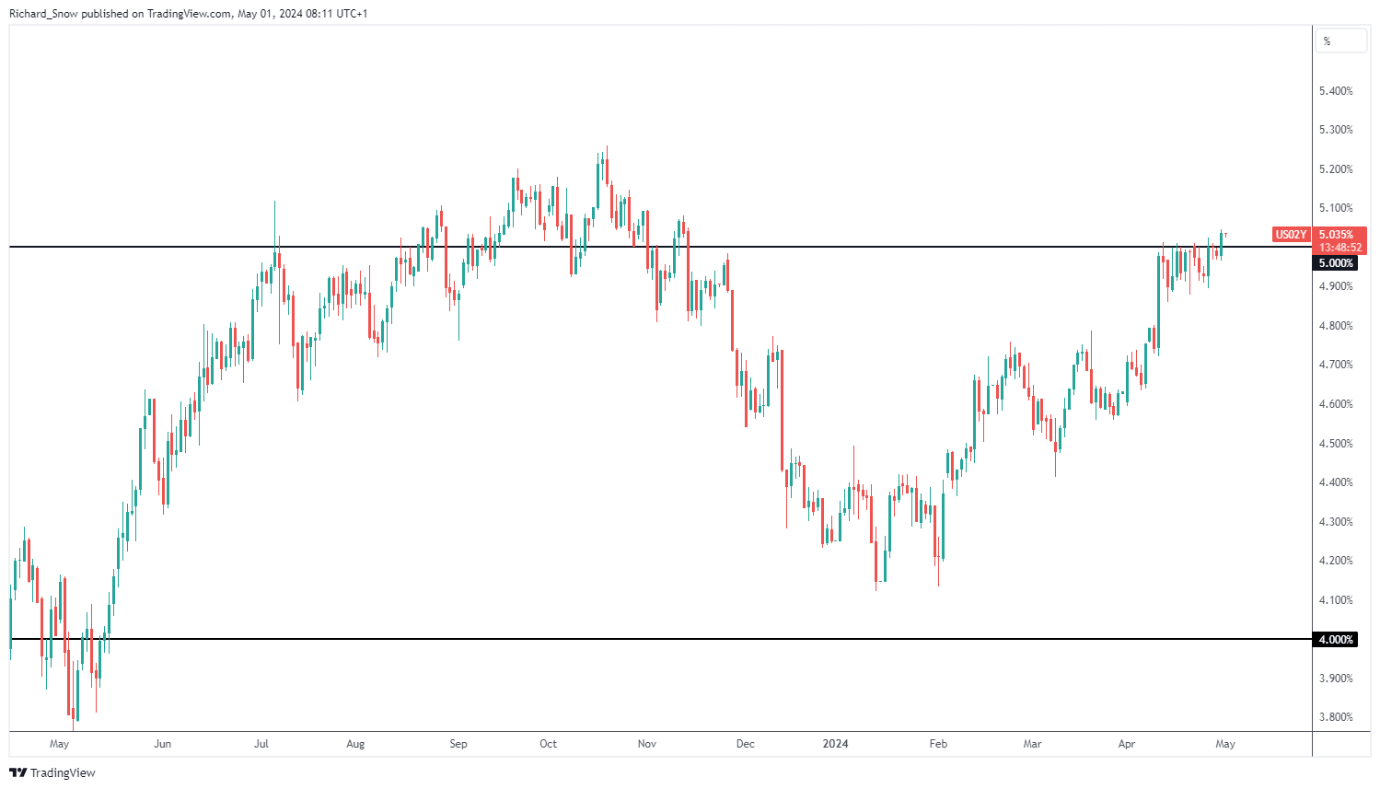

US Treasury Yields Rise – 2Y Breaches 5%

Yields on the shorter end of the curve, like the 2-year yield, have risen and now trade above the 5% marker. Signs of hotter inflation have led the market to delay their expectations of when a rate cut is likely to emerge and have fully priced in a 25 basis point cut in December.

At the end of 2023, markets had priced in between six and seven, while the Fed stands firm on three rate cuts before year end but even this appears optimistic now. US elections in November also complicates the matter further by essentially eliminating a meeting date as the Fed prefer not to move on rates during a presidential election as their was of remaining impartial to politics.

US 2-Year Treasury Yield Daily Chart

Source: TradingView, prepared by Richard Snow

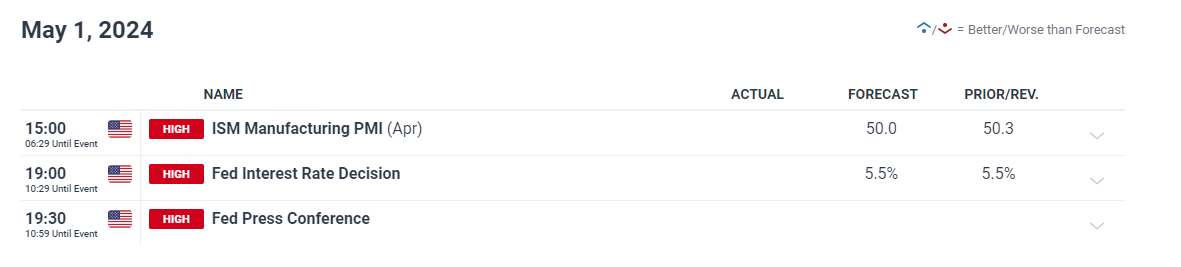

Main Event Risk Today

The high importance data points on the radar today include the FOMC announcement and presser but also PMI data after the flash S&P Global version revealed the sharpest decline in service sector employment since 2009 (not including the Covid decline).

Therefore, keep an eye on ADP payroll data and the hiring rates outlined in the JOLTs report also due today.

Customize and filter live economic data via our DailyFX economic calendar

— Written by Richard Snow for DailyFX.com

Contact and follow Richard on Twitter: @RichardSnowFX

Read the full article here

and Silver (XAG/USD) Drift as US Dollar Pares Recent Losses")

– Repeated Attempts at a Fresh All-Time High, US Retail Sales Weigh")