This guest post is by Vaughn, a long-time Financial Samurai reader who retired at 44 and is now 55. Vaughn’s early retirement was driven by necessity rather than choice due to a congenital bone disease. Fortunately, his high income during his working years secured a solid SSDI benefit, and his mother’s foresight provided future rental income through a duplex. Vaughn shares his approach to maintaining an aggressive 80/20 retirement portfolio with 80% in equities and 20% in fixed income.

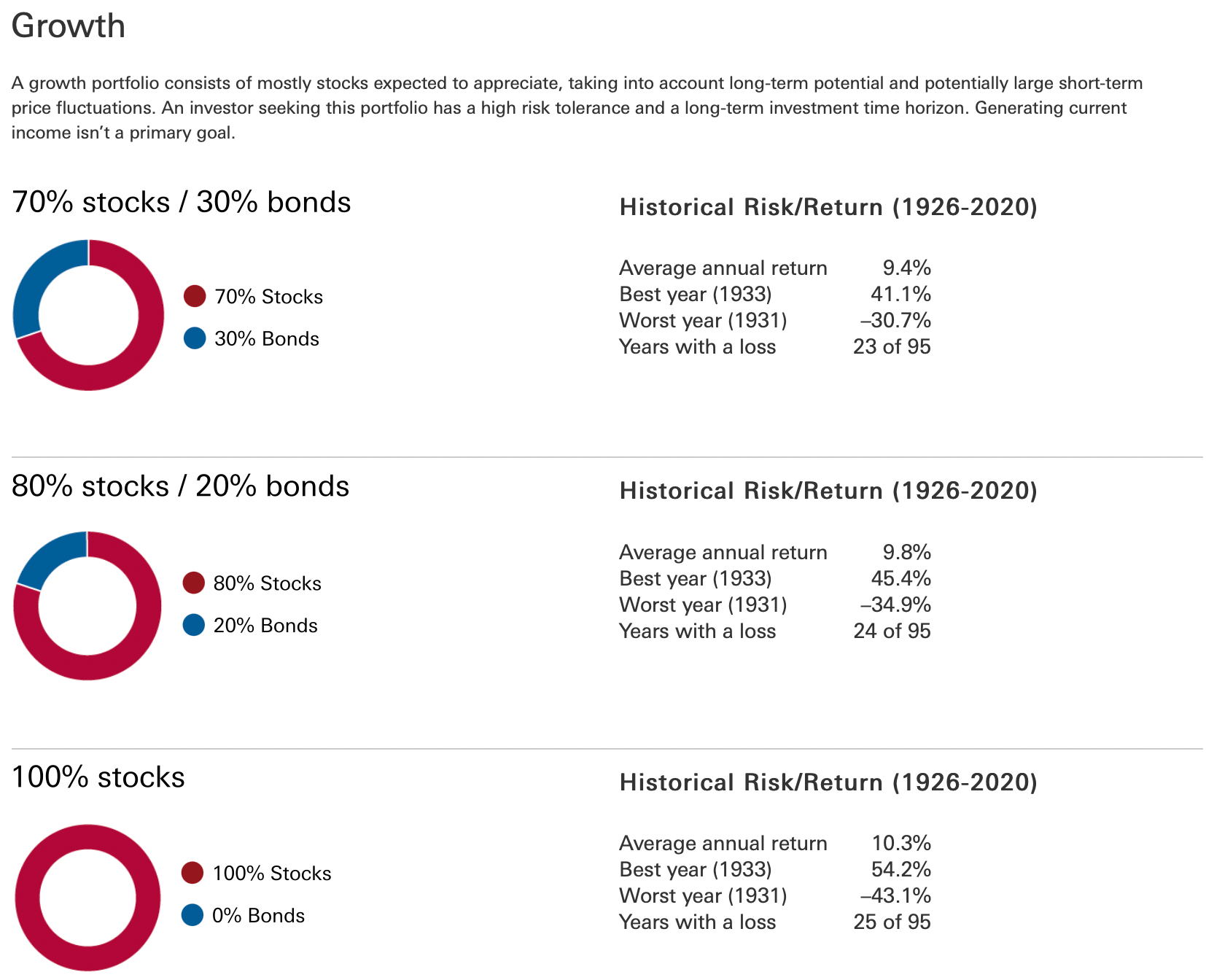

Imagine having an 80/20 stock/bond portfolio in retirement, or an even riskier allocation of 100% stocks. Most would not recommend such an extreme allocation for traditional retirees after the age of 65. But if you’re retiring early, maybe you’ll do just fine.

Living off the dividends of a heavily weighted stock portfolio (80/20) can be a retiree’s best friend, especially if they expect to be retired for a long time. I’m thinking about the would-be centenarian or the FIRE individual who ideally wants their assets to produce indefinitely, starting at an early age.

Let’s first discuss why people would object to a stock-heavy retirement portfolio. Then I’ll argue why the concerns may be overblown.

The Downside Of Having A Heavy Stock Weighting 80/20 Portfolio In Retirement

The cost of this 80/20 retirement portfolio comes in the form of extreme volatility.

Volatility is often defined as risk, but I disagree. To me, true risk is the permanent impairment of capital—losing money for good. Volatility, on the other hand, is just a feature of equity investing.

Next to the risk of losing my capital permanently, inflation is the biggest threat. It’s the risk that my money won’t be worth as much in five years as it is today. Inflation is like a silent killer—slow, creeping, and insidious. You might not even realize you’re in its grip until it’s too late.

Some people catch on early about the ills of inflation, but many don’t realize the damage until it’s already been done. Like any malignancy, early detection is crucial. Waiting too long just limits your options and increases risk even further.

My antidote to inflation, for someone planning for a long retirement, is to heavily weight their portfolio towards equities. Inflation acts as a tailwind for corporate profits, which results in higher profits and higher dividend payouts. The goal is to boost income through dividends rather than relying on a safe withdrawal strategy.

A few years ago, this approach would’ve sounded completely insane to me. So why the change? Because my thinking has evolved. Here are some conclusions I’ve recently drawn.

Living Off Dividends And Supplemental Retirement Income

Despite the volatility of an 80/20 retirement portfolio, I’ve come to realize the following things that have helped me sleep better at night. Perhaps after investing for decades, these reasons may saw you to invest more heavily in stocks as well.

- My emotions deceive me – I used to think volatility and risk were the same because it felt like I was permanently losing money during market downturns. But the markets would eventually recover.

- I assume the worst during uncertainty – When profits dip or there’s talk of a recession, my mind jumps to “Is everything going to zero?!” I’m emotionally irrational at times, but fortunately, I tend to do nothing during these periods. Recently, I’ve gained more awareness of just how irrational I am in moments of uncertainty. That awareness is progress.

- Inflation is real – The past several years truly woke me up to its devastating effects. Inflation has been eroding my purchasing power all my life, but I didn’t take it seriously until the pandemic. I’m grateful for the wake-up call.

- The economy will continue to grow over time – Finding simple ways to align myself with this growth seems like the soundest path to building wealth. All I need to do is get the long-term direction right—up or down?

Patience Is Important As An Aggressive Equity Investor

Though equities are volatile, they tend to have the strongest correlation with economic growth compared to other asset classes. Capitalism is resilient and powerful—there’s no better horse to ride. Broad-based equity exposure is the perfect saddle for the long haul.

If I’m wrong about the economy growing over time, then I doubt any asset class will perform well (except Treasury bonds). My alternative, in times of uncertainty, would be to sit tight and wait for the world to end. But in hindsight, sitting on the sidelines has never proven fruitful.

As long as capitalism remains dominant in the U.S., I believe equity markets will continue to rise over the long term. Therefore, having a much heavier weighting in equities, such as an 80/20 portfolio is logical. Again, capitalism is resilient and powerful—let’s hope we never opt for another economic model.

How I’ve Structured My 80/20 Retirement Portfolio

I like a broad-based index approach that tracks either the world’s economy, the U.S. economy, or both (think VOO, VTI, SCHD, DGRO, or VXUS). I also believe tilting the portfolio toward companies with strong financials and a track record of raising their dividends.

Most importantly, I think a retiree should try and live off the dividends from these broad-based index funds and never sell a share. The benefit is that you’d never need to worry about the right withdrawal ratio or capital gains taxes. You’d simply take whatever dividends capitalism provides. In periods of inflation, you’d likely get a raise, and in economic contractions, your dividend income may take a haircut.

The downside is that you’d probably live off a smaller percentage of your portfolio than what’s customary. But if you can manage this with supplemental retirement income, you’d never run out of money. In addition, your asset base would likely grow over time, along with your dividend income.

If you don’t have rental income to help pay for living expenses like I do, you can always generate supplemental retirement income through part-time work or side hustles. As an early retiree, you will have more time and energy to earn than a traditional retiree.

An Example Of When Dividend Payouts Crashed

During the 2008-2009 Great Financial Crisis (GFC), dividend payouts were cut by about 23%, according to a Barron’s article quoting Goldman Sachs on June 11, 2022, and it took a few years for them to recover. While I wasn’t thrilled with lower income, it coincided with deflation—prices fell, which cushioned the impact.

In 2008, I remember buying Armani ties for $35 at Saks Fifth Avenue in Portland as they prepared to close their doors. A year earlier, those ties were over $100. The irony is that a $100 tie wasn’t in my budget the year before, but thanks to the GFC, I was able to comfortably buy five ties—and an Armani suit I still wear occasionally. Thank you, GFC!

And it’s not just Armani ties that declined in value when the economy imploded, but so did things such as houses, cars, food, and other goods and services. Almost everything traded at a discount.

Depending on your allocation to the ETFs I’ve mentioned, the dividend yield in year one would range from 1.3% to 2.5%. Since I suggest living off the dividends rather than reinvesting them, the more you tilt toward higher dividend stocks, the more your portfolio will likely underperform broader indexes over time.

The 80/20 Retirement Portfolio I’m Building For Myself:

- 70% VOO – This represents the S&P 500 and has a current dividend payout of 1.32%

- 15% SCHD – This tracks the Dow Jones U.S. Dividend 100 Index and has a payout of 3.35%

- 15% DGRO – This represents U.S. Dividend Growers and has a payout of 2.19%

Disclaimer: This is not investment advice for you, but what I’m investing for myself. All your investment decisions and results are yours alone.

Benefits and Specifics of My 80/20 Retirement Portfolio:

- Tax efficient – Nearly all the dividends from these ETFs are qualified. If this were your only source of income, you might not owe any federal taxes, depending on the amount of income generated (for 2024, qualified dividends may be taxed at 0% if your taxable income falls below $47,025 and you’re filling singly. If filing jointly the threshold is raised to $94,050).

- Low cost – The overall cost of the portfolio is around 0.08% annually. Some people overlook the importance of low costs, but by minimizing fees, I’m keeping virtually 100% of the income and gains. If my portfolio fees were 1%, I estimate I’d have $1.2 million less after 35 years. While there’s nothing wrong with paying for active management, it’s not necessary when you’re simply riding the growth of an entire economy.

- Current blended yield – 1.72%

- Rising dividends – The dividends have increased every year for the last decade.

- Inflation-beating growth – Dividend payouts have grown 83% over the last 10 years, far outpacing inflation.

- Capital growth – Despite not reinvesting dividends, the portfolio is still up over 200%.

Related guest post: Overcoming Blindness: Achieving FIRE With A Visual Impairment

Be Cautious About Overconfidence with a Stock-Heavy Retirement Portfolio

The timing of this discussion matters. The market has enjoyed a tremendous run since 2009, especially in the past 24 months, and it’s easy to feel overconfident in a bull market. This can lead to overestimating our risk tolerance.

While my points may be valid, it may not be the best time to fully commit to a stock-heavy portfolio. Instead, consider gradually transitioning to a more aggressive asset allocation if you’re considering a change.

The primary reason I can manage a volatile portfolio is that my daily expenses are covered by Social Security and rental income. The dividends from my investments are used for discretionary spending, like vacations and car expenses. If you don’t have the luxury of such income streams, an 80/20 retirement portfolio might not be suitable.

Personally, I wouldn’t feel comfortable relying on an 80/20 portfolio to cover essential living costs. While capitalism may be the best horse to ride, I’m not eager to take on more risk than I can handle. If you share this concern, a more conservative 60/40 portfolio might be a better fit.

Finally, if you’re still far from retirement, focus on building diverse passive income streams. Even if you choose not to invest aggressively in the future, it’s valuable to have that option.

Readers, what are your thoughts on maintaining an aggressive 80/20 stock/bond retirement portfolio? Given that stocks have historically bounced back, is the fear of permanent capital loss overblown? What are the potential downsides of an 80/20 allocation when Social Security and rental income already cover your living expenses?

– Vaughn

Get A Free Portfolio Checkup

If you have over $250,000 in investable assets, take advantage and schedule a free consultation with an Empower financial advisor here. They can review your existing portfolio construction and see if it is appropriate for your risk tolerance and goals. Complete your two free video calls with the advisor before October 31, 2024, and you’ll receive a free $100 Visa gift card. There’s no obligation to use their services after.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009.

Read the full article here