The markets have gotten off to a roaring start so far in 2024. The S&P 500 is up 18%, while the Nasdaq Composite has gained 23%.

To be honest, investors should be hard-pressed to find a company that is experiencing accelerating revenue, generating profits, and operating in a growth industry whose stock is down this year.

Unfortunately, one company that meets the criteria above is SoFi Technologies (NASDAQ: SOFI). Despite a financially sound business, the stock has cratered 30% so far this year.

Is now a time to buy the dip in SoFi stock, or is the company a falling knife?

Let’s dig into SoFi’s business and explore why now could be a lucrative opportunity for long-term investors to scoop up some shares.

Keep an eye on the lending business

SoFi’s platform offers customers several lending products such as mortgages and business or personal loans, as well as products related to banking and investing.

Despite the company’s end-to-end financial services ecosystem, one area of SoFi’s business appears to be under scrutiny right now: Lending.

During the first quarter of 2024 (ended March 31), SoFi reported net revenue of $581 million — an increase of 26% year over year.

However, the breakdown of SoFi’s revenue is likely what has some investors concerned right now. During the first quarter, SoFi’s lending segment generated $325 million in net revenue. This represented a flat performance year over year. Considering that lending is by far SoFi’s largest revenue generator and the segment essentially experienced no growth during Q1, investors are likely spooked.

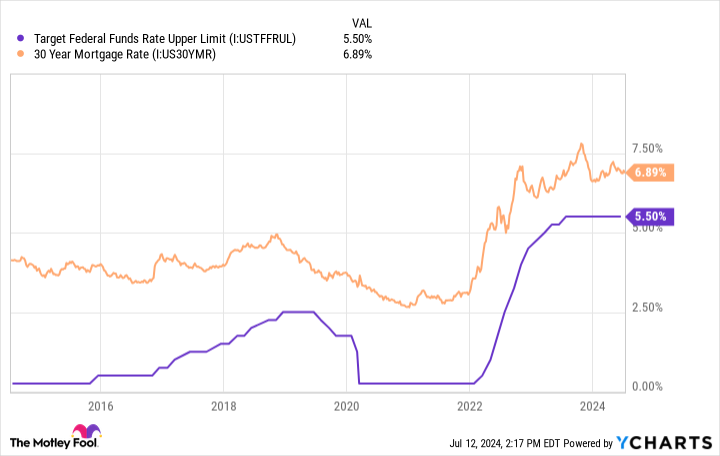

I’d encourage investors to zoom out and consider the broader macroeconomic situation right now. Keep in mind that over the last couple of years, the Federal Reserve has implemented a number of interest rate hikes in an effort to combat inflation.

Given how high interest rates have become, it’s not entirely surprising to see a slowdown in lending services. These dynamics make accessing capital much harder, and consumers and businesses are thinking twice about incurring a high-interest loan right now.

Profits, profits, profits

Although seeing no growth in SoFi’s core lending business seems concerning, I think investors may be missing the bigger picture.

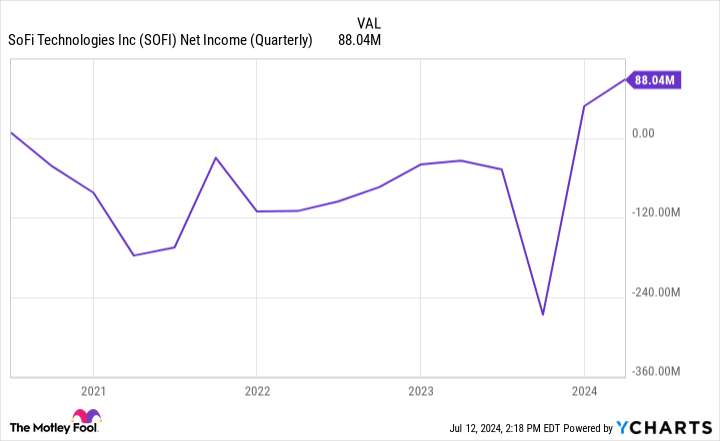

Since going public in 2021, one of the biggest bear arguments surrounding SoFi was that the company is not profitable. Moreover, many investors questioned the company’s aggressive acquisition strategy as it was building out its platform beyond lending products.

These concerns led to doubts that SoFi could evolve from being just another bank, and whether or not sustained profitability was even possible.

As the chart above illustrates, SoFi has finally started generating positive net income on a generally accepted accounting principles (GAAP) basis. While positive net income is still a new theme for SoFi, I find its most recent quarter of profitability even more impressive considering its biggest business (lending) didn’t even grow.

A compelling valuation

The one aspect of investing in SoFi that is so difficult is valuation.

If the company truly is just a bank, then the price-to-book (P/B) multiple would probably be a good measure to use. However, considering that SoFi has a large and growing tech-enabled business thanks to its acquisitions of Galileo and Technisys a few years ago, I think viewing SoFi as a bank is shortsighted.

With that said, I also think valuing SoFi on a price-to-earnings (P/E) basis doesn’t make a ton of sense at the moment, considering GAAP profitability is a relatively new thing for the business.

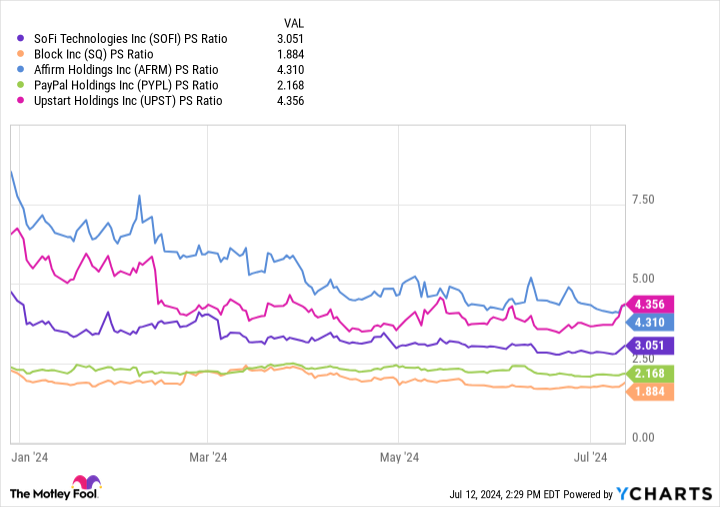

In the chart below, I’ve benchmarked SoFi against other financial technology (fintech) solution providers using the price-to-sales (P/S) multiple.

With a P/S of 3.0, SoFi is valued right in the middle of the pack of this peer set. By looking at the trends above, investors can see that many of these fintech stocks have actually witnessed some compression in their multiples since the start of the year.

Bearing that in mind, I think these trends undermine the sentiment surrounding financial services more broadly at the moment. Stated differently, the sell-off in SoFi doesn’t appear to be specific to the company.

It’s important to remember that the Federal Reserve will eventually cut rates. Whether it happens later this year or not, it’s safe to say that borrowing costs will not rise forever.

As the macro picture normalizes, I think SoFi will experience an uptick in lending products, which should contribute even more to the company’s already impressive revenue growth and profit generation. Given its valuation compared to peers, newfound profit generation, and a lending business poised for a comeback, I think now is a great opportunity to scoop up shares in SoFi.

Should you invest $1,000 in SoFi Technologies right now?

Before you buy stock in SoFi Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoFi Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $791,929!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of July 8, 2024

Adam Spatacco has positions in Block and SoFi Technologies. The Motley Fool has positions in and recommends Block, PayPal, and Upstart. The Motley Fool recommends the following options: short September 2024 $62.50 calls on PayPal. The Motley Fool has a disclosure policy.

Down 30%, Is Now a Good Time to Buy the Dip in SoFi Stock? was originally published by The Motley Fool

Read the full article here