Empower is offering free financial consultations until October 31, 2024, for anyone with over $250,000 in investable assets. I wanted to share my experience speaking with them and how I began my investing journey. If you complete two video calls by the deadline, you’ll receive a free $100 Visa gift card. There is no obligation to use their services afterward.

The Start Of An Investing Journey

I’ve been a DIY investor since 1995 when I first opened an Ameritrade account with my dad’s help. The year before, he had sat me down at the breakfast table and explained what the various ticker symbols meant at the back of the local newspaper. I was fascinated.

I started with $500 in my online brokerage account, mostly money I earned working at McDonald’s for $4 an hour. Then, like a coke fiend chasing his next hit, I dove into day trading. Within six months, I lost most of my money.

All those hours standing in front of a hot stove making Egg McMuffins and Big Macs were for nothing! I wish I could have spoken to a financial advisor to give me some guidance. My dad was good at telling me about the basics of stocks. But he didn’t explain to me how to invest or the purpose of investing.

As a father now, I also realize kids often listen to an instructor more than their parents. I can’t tell you how many times I brushed off my wife’s advice, only to agree later after listening to an expert share their same thoughts online!

The Rise of the Stock Market Addict

You’d think I would have learned my lesson in high school and college about the dangers of day trading. But no, my stock market addiction only worsened after joining the International Equities desk at Goldman Sachs. But I’m not sure it was entirely my fault.

According to addiction experts, the inputs that push people toward addiction are: volume, accessibility, novelty, and intensity. Once I graduated from college, I was hit with all four all at once!

I worked on the 49th floor of One New York Plaza, NYC. While sitting high above, phones rang non-stop as sales traders took orders from institutional clients. The buzz on the trading floor would start around 6:45 am and crescendo into a frenzy by the close at 4 pm.

If you’re addicted to donuts, living next to a donut shop will be the death of your diet. But I wasn’t just living next to the shop—I was on the assembly line, glazing the dough all day with maple frosting! And every day there were multiple flavors to try.

Unfortunately, I became hooked on stock trading once again. This habit ultimately turned into a career-limiting move at my next job at Credit Suisse when I joined in 2001.

You Are Not Smarter Than the Market—Stop Trading

For the love of God, please do not day trade stocks. You might get lucky sometimes, but without proper risk management and emotional control, you will eventually lose your shirt. There’s a reason the average retail investor underperforms the S&P 500 and other asset classes over time.

I remember one year, I day traded over $10 million in stock volume. For all my effort, I might have made $12,000. The head of the International Equities department flew over to San Francisco from NYC and sat me down. He basically asked, “What the hell are you doing? Focus on your job.”

That was likely the beginning of the end of my career. To get promoted to Managing Director, I needed buy-in from a committee of MDs, including the head of International Equities.

After playing hardball with management for a big raise in 2011—and getting it because I was being lured away by an upstart competitor—I got zeroed in 2012. That’s when I decided to negotiate a severance package and leave finance behind for good.

A Financial Professional Helped Cure My Addiction To Trading

In early 2013, when Empower was still called Personal Capital, I had an in-person meeting with one of their financial professionals at their San Francisco office. As a Registered Investment Advisor (RIA), they were offering a free financial consultation at the time, much like they are today. So I figured I’d take advantage of it. I was already using their free financial tools and planned to consult with them part time.

Given my significant life change of being a 35-year-old unemployed man, I wanted a second opinion on my portfolio. I was still scarred by the global financial crisis of 2008-2009, which had cut my net worth by 35% – 40% in six short months.

Since 1996, I had developed a dangerous mindset, thinking I was smarter than the markets. Without a steady paycheck to make up for any future stock losses, I finally had to seek help. This is where Patrick, my financial advisor, came in.

Received An Intervention From My Financial Professional

During our consultation, he reminded me of the benefits of long-term investing. When he discussed tax-loss harvesting, he pointed out the inefficiencies of paying short-term capital gains taxes. And perhaps most beneficial was showing a pro forma chart, highlighting what I could potentially have in my investments in the future if I changed my asset allocation.

I knew of all this given my background in finance, but it took someone to tell it to my face while I was going through a significant period of uncertainty to make a change.

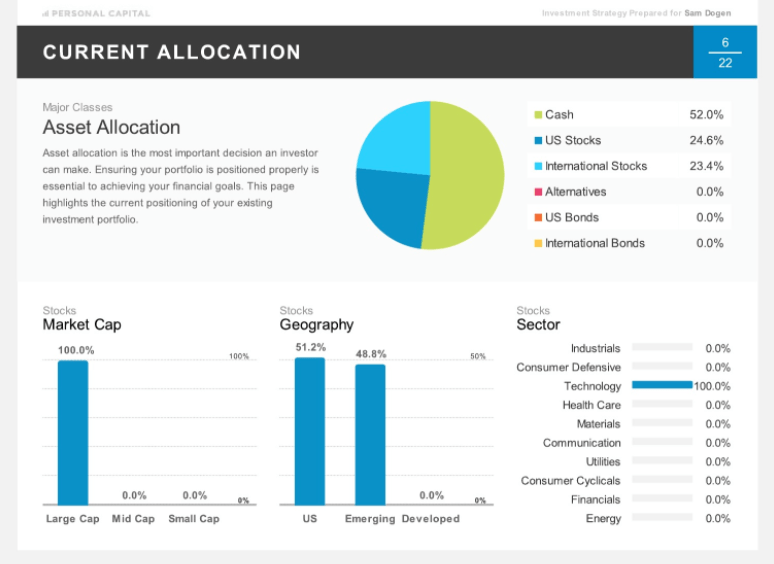

A Blind Spot My Financial Professional Showed Me

Below is a chart of my asset allocation in one of three portfolios back in 2013. It had a little over $500,000 in it. What stands out to you?

You’re correct about the 52% allocation to cash (~$255,000) and 100% allocation to tech stocks! Looking back, I initially couldn’t believe I had such a large amount of cash. However, it made sense at the time because I no longer had a job. 95% of the cash was in CDs yielding an average of about 4.5%, so it wasn’t terrible. But still.

During the height of the 2009 financial meltdown, I remember buying 5-year and 7-year CDs because I was scared. I feared not only losing all my money in stocks and real estate but also losing my job.

The only two good things I did during the global financial crisis were:

- Not selling existing positions

- Starting Financial Samurai in July 2009

The fear of being broke and unemployed finally pushed me to launch this site, which I had first conceived in 2006 after graduating from business school. Unfortunately, I don’t remember buying a significant amount of stocks during the global financial crisis.

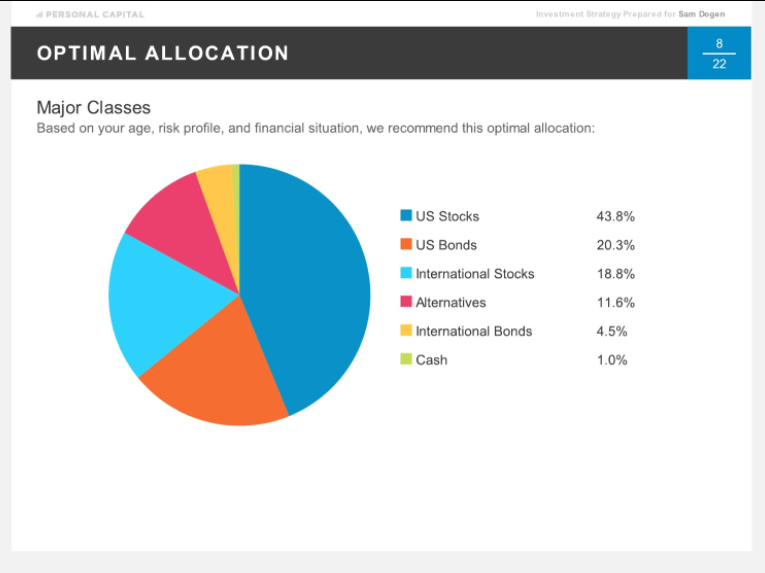

My Financial Professional Reminded Me I Was Still A Young Man

During my second session with an Empower financial professional, Patrick suggested an asset allocation tailored to my age (35), risk tolerance, and goals.

Initially, I resisted this recommendation because I was focused on living a minimalist retirement on my grandfather’s farm in Waianae, Oahu. In my mind, I was a 35-year-old retiree who needed to invest conservatively, just as any traditional 65-year-old retiree would. I was happy with my net worth and ~$80,000 a year in passive income at the time.

I didn’t retire from finance to start a career as an internet entrepreneur. All I wanted was to kick back and continue writing on Financial Samurai and potentially write more ebooks after How to Engineer Your Layoff became a success. If I could make $1,000 a month in supplemental retirement income online to pay for mangoes, boogie boards, and tennis equipment, I’d be thrilled..

In other words, I felt I had to be super conservative with my investments because I had no other choice. My active income was squashed, as so was my energy to return to work. I just needed to preserve as much capital as possible to never experience the hellish conditions of 2009 again.

Finding The Courage To Take More Risk

In the financial professional’s mind, I was still a young man with plenty of energy and many financial opportunities ahead. This concept of FIRE (Financial Independence Retire Early) in 2013 was still a fringe concept, even though I had been writing about it since 2009. Therefore, I could afford to take on more risk—certainly more than having 52% of my portfolio in cash.

While I didn’t follow his recommended optimal allocation exactly, the consultation did motivate me to invest all of my idle cash within a year.

Invested $150,000 Of My $255,000 In Cash In Stocks In 2013

The S&P 500 in mid-2013 was trading around 1,600. Given the S&P 500 is at about 5,800 today, investing ~$150,000 in the S&P 500 and various tech stocks has proven to be a good move. $150,000 in the S&P 500 has grown to over $600,000 today.

Invested The Remaining $100,000 + Expiring CD Into Real Estate In 2014

The following year, I used my remaining $100,000 cash plus 100% of an expired CD for a down payment on a fixer-upper in Golden Gate Heights, San Francisco in 2014. The house cost $1.24 million and had panoramic ocean views on a double lot.

I put $248,000 down, then I took out a $992,000 mortgage. At the time, I recognized the real estate market had begun creeping up since 2012 and I wanted more exposure. I couldn’t believe ocean view homes were selling at such steep discounts.

Taking on a new $992,000 mortgage without a day job and with a wife eager to retire early was far from conservative! However, without W2 income, qualifying for a mortgage would have been impossible. So we decided to go all in before my wife retired in 2015. To improve cash flow, we rented out our previous house, which was 70% more expensive.

At the time, I had been wanting to return to Hawaii and see the ocean for two years. Buying this house was my hybrid solution. I’d build a deck off the main bedroom and enjoy Hawaii in San Francisco.

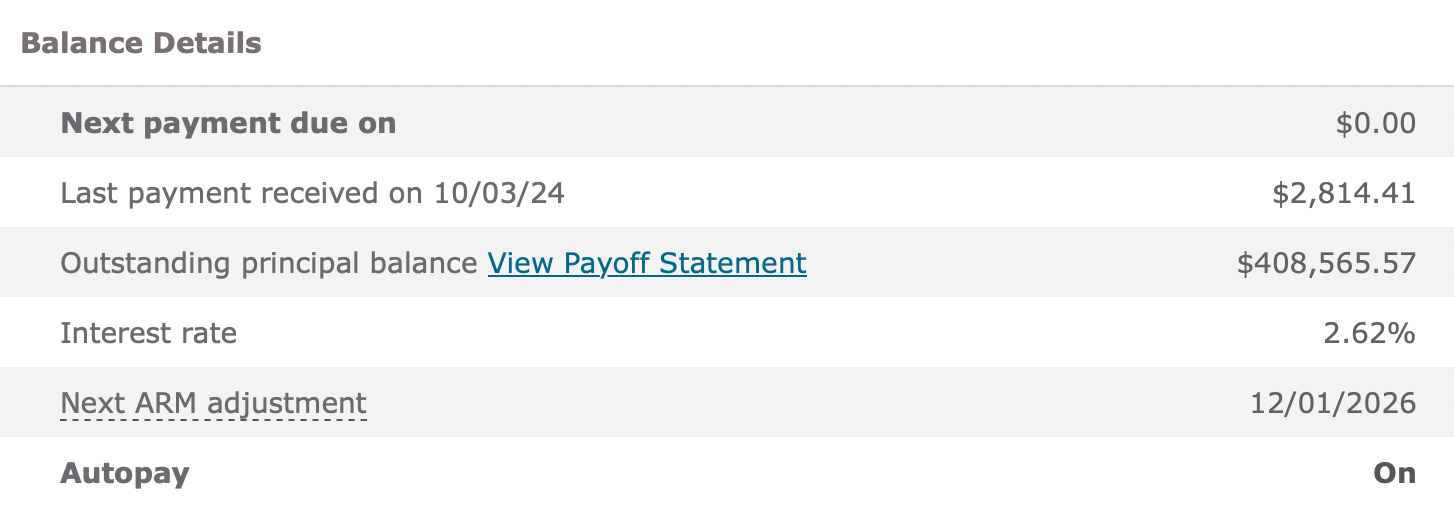

A Neighbor Just Sold At A Healthy Price

It’s been 10 years since the home was purchased. The remaining mortgage balance is still $408,585. But ever since refinancing it to a 7/1 ARM in 2019, I haven’t been motivated to pay down a 2.62% mortgage.

Recently, a neighbor’s property with inferior views, no deck, no hot tub, a terraced backyard, 240 square feet less living space, a 1,400 square foot smaller lot, and an outdated remodel sold for $2.25 million.

This indicates that the $248,000 down payment has grown to over $1,250,000 in equity, excluding the $583,435 paid down on the mortgage. Including the mortgage paydown, the equity has increased from $248,000 to $1,840,000 before fees and transfer taxes if I were to sell.

Who Should Speak To A Financial Professional

A financial professional didn’t directly turn my $255,000 in cash from 2013 and $150,000 from an expired CD in 2014 into $1,850,000. However, he did help give me the confidence to start investing more aggressively. Back in 2013, I was still in a defensive mindset, even though I was only 35 and had my whole life ahead of me.

If I hadn’t spoken to a financial professional, I likely would have deployed my cash much more slowly and conservatively—or perhaps not invested it at all. By mid-2015, my wife had also left her job, which could have made me even more hesitant to take investment risks.

Consider speaking to a financial professional if you’re experiencing the following:

- Major Life Events: Significant changes like marriage, having children, buying a home, or receiving an inheritance are good times to consult a financial professional. They can help you adjust your financial plan to accommodate new responsibilities or opportunities.

- Approaching Retirement: As you near retirement, it’s crucial to ensure that your savings and investments will support your desired lifestyle. A financial advisor can help you transition from saving to generating income. They can also help you decide on the most tax-efficient asset sale strategy.

- Complex Financial Situations: If you have multiple income streams, own a business, or have substantial assets, a financial advisor can help you navigate complex financial decisions. This includes tax strategies, estate planning, and risk management.

- Lacking Time or Expertise: If you don’t have the time or knowledge to manage your finances effectively, an advisor can take on this responsibility, allowing you to focus on other aspects of your life.

- Facing Financial Challenges: If you’re dealing with financial uncertainty or want to optimize your financial health, a financial advisor can provide guidance and strategies to improve your situation.

- Planning for the Future: Whether it’s for retirement, education expenses, or long-term care, a financial advisor can help you create and maintain a plan to achieve your goals. The continuity of a plan is important as the financial advisor gets to know about you over time.

- Desire for a Second Opinion: Even if you’re confident in your financial plan, getting a second opinion from a professional can provide peace of mind or highlight areas for improvement.

If any of these scenarios apply to you, speaking to a financial professional is a wise decision. Financial professionals review portfolios and speak to people like you all the time. It’s good to get some insights into what other people in your similar situation are doing with their money.

Questions To Ask A Financial Professional

If you decide to get a free consultation with an Empower financial professional, here are some questions I’d ask:

- How are other investors with a similar profile to mine currently investing?

- What are the biggest concerns for investors with my profile at the moment?

- What is the average cash balance for investors like me?

- How do you anticipate the investing landscape might change under a Harris or Trump presidency?

- How do you expect your recommended asset allocation for me to perform relative to the S&P 500?

- What are your thoughts on the benefits of direct indexing and tax-loss harvesting?

- How should real estate factor into my portfolio?

- How large could my investments grow over a 5, 10, 15, and 20-year period?

- Do you think it’s better to invest my cash in one lump sum or dollar-cost average over time?

- What is the value proposition of your product?

Don’t expect your financial professional to know the answers to all your questions. However, based on their responses, you should be able to gauge their expertise and the quality of their product offerings.

I don’t rely on a financial professional solely for investment advice. Instead, like a personal trainer, I rely on a financial advisor to keep me accountable in executing my financial plan.

Make Sure You Have A Financial Plan

Ten years will fly by before you know it. So it’s crucial to develop a financial plan and stick to it. By doing so, you’ll likely come out way ahead compared to those who don’t. Consult with a trusted expert to help you gain more freedom in the future.

For those with over $250,000 in investable assets seeking a free financial checkup, you can schedule an appointment with an Empower financial professional here. If you complete your two video calls with the advisor before October 31, 2024, you’ll receive a complimentary $100 Visa gift card, with no obligation to sign up afterward.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”). Click here to learn more.

To increase your chances of achieving financial independence, join 60,000+ readers and subscribe to my free Financial Samurai newsletter here.

Read the full article here