Aurobindo Pharma (NS:) has outperformed expectations in the fourth quarter of FY24, with both sales and EBITDA showing significant year-over-year growth. Sales increased by 17%, while EBITDA surged by an impressive 68%, surpassing both Goldman Sachs (NYSE:)’ projections and those of the broader market.

This robust performance was driven by strong growth across key geographical markets, both developed and emerging. The EBITDA margin also exceeded forecasts, reaching 22.3%, which is 101 basis points higher than Goldman Sachs’ estimate. This improvement was primarily attributed to higher gross margins.

Offer: Now’s the perfect time to seize the opportunity! For a limited time, InvestingPro is available at an irresistible discount of 69%, priced at just INR 216/month. Click here and don’t miss out on this exclusive offer to unlock the full potential of your portfolio with InvestingPro+.

Although Aurobindo did not provide a specific consolidated topline growth guidance, the company remains optimistic about achieving solid growth in FY25. This optimism is underpinned by several factors, including sustained momentum in the US market, substantial growth in Eugia (with a target of $150 million quarterly run-rate), and an anticipated ramp-up in gRevlimid sales in the coming quarters.

The company’s Production Linked Incentive (PLI) project is on track, aiming for peak utilization by September. Additionally, Aurobindo plans to commission its China plant this year and expects to maintain an EBITDA margin of 21-22% in FY25.

Goldman Sachs has adjusted its EPS estimates for FY25-27 by a range of -3% to +4%, reflecting the latest quarterly performance and updated business outlook. Consequently, the 12-month sum-of-the-parts (SOTP) target price for Aurobindo has been raised to INR 1,325 from INR 1,275, indicating an 11% upside potential. The firm maintains its Buy rating on Aurobindo, noting that the current valuation, which trades at a 30-40% discount to the coverage average, alleviates most concerns regarding pricing pressures and plant status.

In Europe, Aurobindo’s revenues grew by 8% year-over-year and 5% quarter-over-quarter, reaching EUR 203 million. This growth was in line with the company’s guidance and was helped by a reduction in tax clawback impacts. The company aims to maintain this revenue run-rate in FY25 and is focused on improving margins from the mid-teen levels to around 20% in the medium term.

Image Source: InvestingPro+

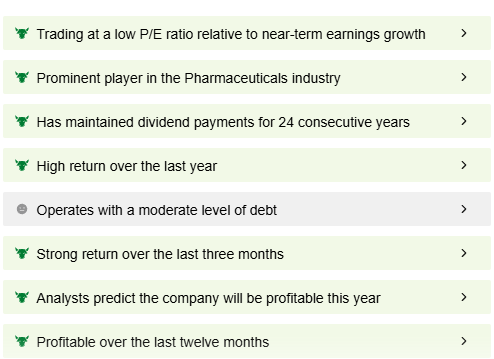

In addition to Goldman Sachs’ analysis, InvestingPro offers valuable insights into Aurobindo Pharma’s stock. According to InvestingPro’s fair value calculation, the true worth of the stock is INR 1,270. This valuation is derived from complex financial models that provide a comprehensive analysis of the stock’s potential. InvestingPro’s ProTips feature further underscores the stock’s attractiveness by highlighting its consistent 24-year dividend payout history, its low price-to-earnings (P/E) ratio, and its profitability over the last 12 months.

Image Source: InvestingPro+

For investors seeking a deeper understanding and actionable insights, InvestingPro stands out as a powerful tool. By clicking here and subscribing to InvestingPro, investors can get access to a wealth of information and tools that can help them make informed decisions, maximizing their potential returns in the stock market, now available at a 69% limited-time discount.

Also Read: Boost Your Investment Strategy with the Altman Z-Score

X (formerly, Twitter) – Aayush Khanna

Read the full article here