Investors trust Warren Buffett for a reason. Although he’s the first to say he’s made mistakes, he has a proven track record of picking winners and beating the market.

One of his more curious picks is Nu Holdings (NYSE: NU). That’s not because Nu isn’t a great stock; it’s up 54% this year, and it’s reporting incredible results. It’s unusual because it’s a growth stock in a risky region, which isn’t usually Buffett’s style.

If Buffett’s bullish on this stock, though, it may not be as risky as it seems. And at under $15 per share, it could be a bargain. Let’s dive in and see.

What Nu has already done

Nu operates under the NuBank banner as an all-digital bank in Brazil, Mexico, and Colombia. It has quickly emerged as a real challenger to the traditional banks in these regions, capturing market share and demonstrating impressive results.

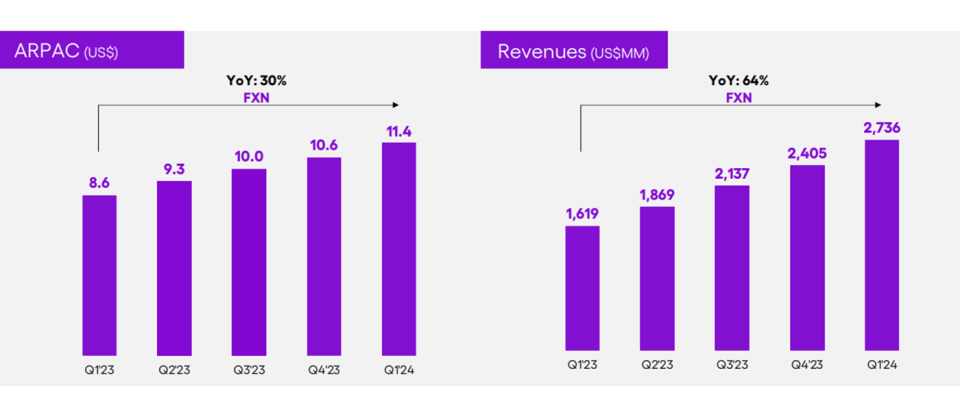

Nu is a fast-growing organization and is reporting strong operating metrics across the board, but it’s focused on three key goals: Adding customers, expanding revenue per customer, and scaling efficiently. Its quarterly updates consistently show progress in these areas, and it continued in the 2024, adding 5.5 million customers in the first quarter and ending it with 99.3 million.

The company is still mostly concentrated in its core region and headquarters of Brazil, where there were 1.3 million new customers monthly. It has 54% of the adult population of Brazil on its platform and has moved up to the become the fourth-largest bank in the country by number of members.

Still, Nu also added 1.5 million members in Mexico, ending the quarter with 6.6 million, or 106% more than last year. It only has 900,000 members in Colombia, its newest region, and it’s still rolling out products there.

Average revenue per active customer (ARPAC) is one of Nu’s most important metrics, and it continues to expand quarterly. This measures engagement and organic growth, both of which, combined with new customers, lead to total revenue growth.

As for efficient scaling, Nu turned profitable a few years ago and has maintained and grown its net income. As an all-digital bank (which means no real estate), with increasing revenue per customer (which means less marketing expense), it’s keeping its expenses low. Cost to serve (an accountancy measure) has remained relatively stable over the past few quarters, coming in at $0.80 or $0.90 per active customer.

Where Nu is going

Nu has several objectives to keep making its growth a reality. It has four key priorities for 2024: getting deeper into Mexico, expanding its credit business in Brazil, targeting an upscale market in Brazil, and upgrading technology to offer better products.

Not only is Nu adding millions of members in Mexico, but at 19 quarters into its Mexico launch, many key performance indicators are outpacing how it did in Brazil at 19 quarters in. It has more customers in absolute numbers and percentage of market, more credit card customers, and more credit card purchase volume, and many more metrics show similar results.

Its credit segment in Brazil is outdoing overall market averages, and the total portfolio increased 52% year over year. Loan originations were up 95%, and growth in the interest-earning portfolio is driving net interest income growth and net interest margin expansion.

Nu is capturing greater market share in the high-income segment, with 2023 purchase volume up 104% year over year, and the highest net promoter scores in the industry. It recently launched a short film in partnership with Walt Disney to attract interest from this population.

Is it a bargain at under $15?

As most investors know, identifying a bargain stock has more to do with the stock’s valuation than its price tag. There are a variety of tools to assess valuation, and some work better than others for different stocks.

Nu Holdings is a bank, but it’s a high-growth-fintech kind of bank. It’s way more expensive than the traditional, established bank when using a price-to-book value, and it’s also more expensive using a price-to-earnings ratio. But it’s actually much cheaper when using a forward one-year price-to-earnings growth (PEG) ratio, because it’s growing so fast.

A company reporting growth as high as Nu with stable and increasing earnings gets a premium on its stock. Its price-to-earnings ratio of 49 might be expensive for a bank stock, but cheap for a high-growth stock. So while it may not look like a bargain in the traditional sense, its valuation doesn’t seem unreasonable.

Nu stock trades at $12.80 as of this writing, and it looks like a strong buy for growth investors with some appetite for risk.

Should you invest $1,000 in Nu Holdings right now?

Before you buy stock in Nu Holdings, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nu Holdings wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $805,042!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of July 8, 2024

Jennifer Saibil has positions in Nu Holdings and Walt Disney. The Motley Fool has positions in and recommends Walt Disney. The Motley Fool recommends Nu Holdings. The Motley Fool has a disclosure policy.

Should You Buy Nu Holdings Stock While It’s Below $15? was originally published by The Motley Fool

Read the full article here