Taiwan Semiconductor Manufacturing Company (NYSE:TSM), or TSMC, is one of the best-rated mega-cap stocks by analysts on TipRanks. It’s rated a Strong Buy, with 10 Buy ratings and no Sell or Hold ratings. However, the stock has surged since I last covered it on April 29, and despite several positive catalysts, I’m only somewhat bullish on TSM, with the valuation becoming increasingly stretched. Therefore, it may not be the best opportunity out there despite the Strong Buy consensus rating.

TSMC Surges

Since I last covered TSMC stock, it has surged 38%. That’s just in eight weeks. The stock has been pushed higher by investors’ insatiable demand for companies involved in the development of artificial intelligence (AI) as well as several bullish analyst updates.

This built on stronger delivery figures in the spring, with a 60% surge in April sales to $7.3 billion. That’s a huge increase in anyone’s books. TSMC had already registered a 34.3% increase in revenue growth in March. Unsurprisingly, this was fueled by the relentless demand for AI semiconductors.

The Taiwanese company’s share price has also benefited from its strategic partnerships in recent months, including with Nvidia (NASDAQ:NVDA). TSMC is the exclusive producer of Nvidia’s most advanced training chips, which are continuing to generate exceedingly robust demand, according to Wall Street analysts.

Moreover, recent data put to bed concerns that hyperscale demand would dip during the transition between Nvidia’s current Hopper series products and its upcoming Blackwell series products. The graphics processing units used in the Blackwell architecture are manufactured using a custom-built 4nm TSMC processor.

Geopolitics and Geography Remain Issues

TSMC, the world’s largest contract chipmaker, faces significant geographic concentration risk, and this has long been a concern for investors. Taiwan’s susceptibility to natural disasters, particularly earthquakes, poses a threat to TSMC’s operations, as was demonstrated earlier in 2024. Additionally, escalating tensions with China, which asserts sovereignty over Taiwan, continue to amplify geopolitical risks.

In response, TSMC is diversifying its manufacturing footprint by constructing and ramping up new foundries in Japan, the U.S., and Europe. This strategic expansion reduces the concentration risk associated with Taiwan’s geopolitics and geography.

However, building and operating fabs (semiconductor manufacturing facilities) overseas incurs higher costs due to varying regulatory environments, labor costs, and supply chain logistics. Moreover, Taiwan offers huge economies of scale as a global foundry, and this isn’t being strategically utilized when building fabs overseas. Consequently, customers are likely to face premium pricing for chip production in these regions, particularly in the U.S. and Germany.

TSMC’s Evolving Market and Margins

The AI revolution has significantly influenced TSMC’s market, driving demand for smaller, high-end processors and chips. This is because AI applications require more advanced processing capabilities. This trend is particularly evident in the 3nm and 5nm segments, which comprised 9% and 37% of TSMC’s FQ1’24 revenues, respectively.

The Taiwanese chip giant has already raised prices moderately, buoyed by the fully booked 3nm capacity through 2026. This price adjustment also aligns with TSMC’s goal of maintaining a long-term gross margin of 53%.

Moving forward, analysts have suggested that more price hikes could be on the table with the cost of electricity, materials, chemicals, gases, and other variables rising in Taiwan. Rising costs are expected to impact gross margins by up to 70 basis points from FQ2’24, while the conversion of 5nm tools to support 3nm demand has already impacted margins by 200 basis points.

TSMC’s Valuation Is Getting Stretched

TSMC used to be dirt cheap. I held the stock for some time, and it was trading in line with the average price-to-earnings for the downtrodden FTSE 100 Index. However, it’s now looking a bit more expensive at 29.3x forward earnings and with a price-to-earnings-to-growth (PEG) ratio of 1.21x (1.0x or lower is generally seen as undervalued). While this PEG ratio is cheap for the sector, it all depends on the discount we attribute to TSMC’s geographical challenges.

What Is the Price Target for TSM Stock?

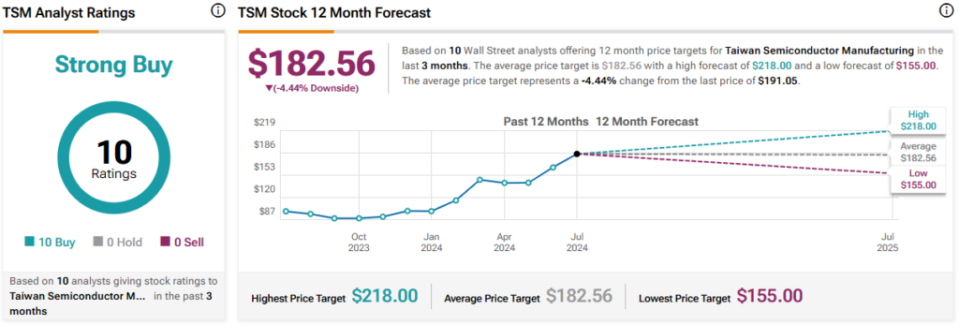

On TipRanks, TSM comes in as a Strong Buy based on 10 Buys, zero Holds, and zero Sell ratings assigned by analysts in the past three months. The average TSMC stock price target is $182.56, implying 4.44% downside potential.

However, it’s worth noting that all share price targets have been above the share price at the time of issue — hence why all the ratings are Buys. The last five ratings have share price targets in excess of the current share price.

The Bottom Line on TSMC Stock

I remain somewhat bullish on TSMC stock. However, I believe the valuation metrics are starting to become a little stretched when taking into account the geopolitical and geographical issues that the companies face. To some extent, I think investors are electing to discard this vital consideration, which marks a stark change from 18 months ago when it was front and center.

Disclosure

Read the full article here